The current economic housing market conditions affect every age group, but we have seen that it significantly affects the young Gen X, millennials, and Gen Z generations. The pathway to wealth starts with homeownership. Owning a home builds equity over time through appreciation. If you can buy a home, you are in great shape in framing a future of financial stability. Because home prices have skyrocketed in the last 4 years due to inflation and lack of inventory due to high mortgage rates, many are unable to get into the wealth-building of homeownership. If you are a young American who has been able to purchase a home or investment property, you are in the minority and on record have more equity than past generations because of the high home prices. However, the majority of young American’s have been iced out of homeownership and forced to lease at astronomical rents. As a result, young Americans do not have a favorable climate to put them on the path to wealth building through homeownership.

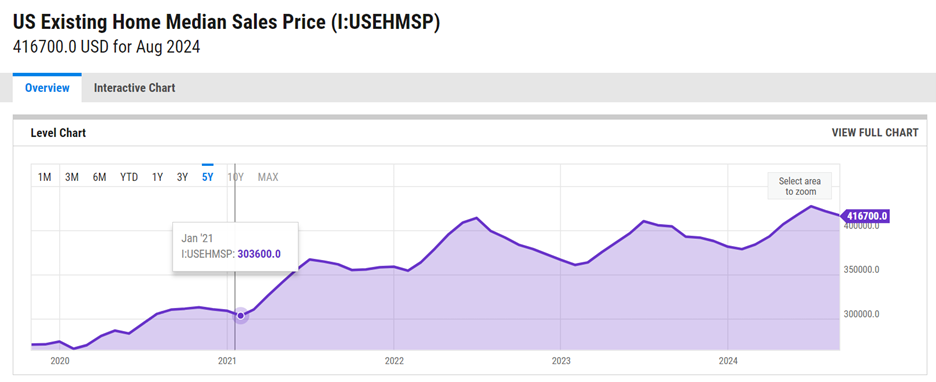

Housing affordability has been stifling for young Americans and/or first-time homebuyers. As per Y-charts from January 2021 to August 2024, median U.S. home prices have risen by about 30% from $304,000 to $417,000.1

At a micro level, the home prices have risen even more drastically. For example in NJ, home prices have essentially doubled.

Inflation and high yield rate have caused mortgage rates to rise creating a lock-in effect for home sellers who do not want to sell their homes, causing the low housing inventory with higher demand, causing home prices to rise, and ultimately drastically reducing the affordability for prospective homebuyers. The latest statistics show that affordability of first-time homebuyers and young Americans decreased to 62%, meaning that the income of first-time homebuyers is only 62% of what is needed to qualify to purchase a home. Wealth-building through homeownership is out of reach for young Americans.

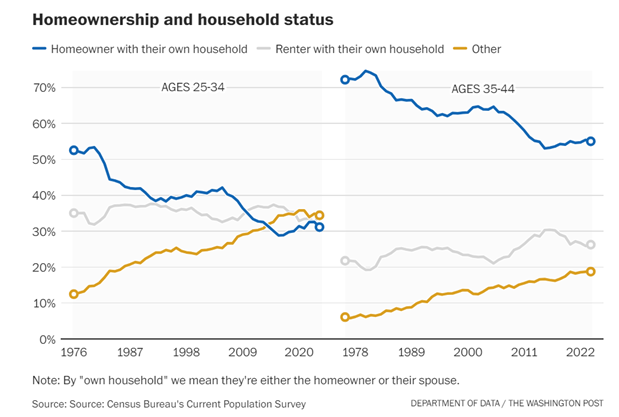

Some are trying to spin that young Americans have more equity built in comparison to their parents when they were the same age. If you are a young American that was fortunate enough to have the finances to buy a home in recent years, then consider yourself lucky. Equity is artificially higher in comparison because of the exorbitant home prices. On the other hand, due to low affordability, young Americans aged 25-34 and 35-44 are owning less homes and renting more leases than past generations.2 Therefore, the overall equity is lower amongst the young American generations.

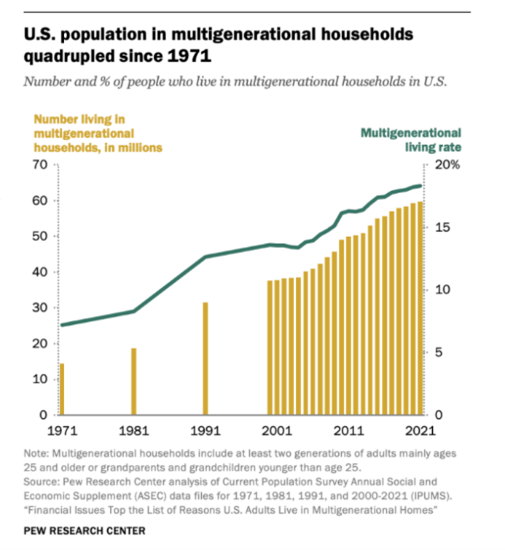

Multigenerational homes have been increasing consistently primarily due to high housing costs and student debt.3

Young Americans are opting to stay at home with their parents as an alternative to renting. These stay-at-homes are not counted in the calculations of homeownership or renters, underestimating the lack of affordability and inflating of equity. Of those in multigenerational households, 72% say that they plan on continuing to do so for the long-term.4

In summary, young Americans and first-time homebuyers continue to be suppressed by the current economic conditions. Although on the surface it appears that they accrued more equity through homeownership than past generations, a more detailed examination shows that the number is skewed because of the high home prices. Financial strains due to the lack of affordability is causing fewer young Americans to begin their wealth building journey of owning a home. The high inflation and mortgage rates are not providing any relief in site and multigenerational households are here to stay until we can get back to policies that restore economic health.

1 https://ycharts.com/indicators/us_existing_home_median_sales_price

October 13, 2024

By Sophia Georges

Copyright 2024 - Realsophy Real Estate, Sophia Georges